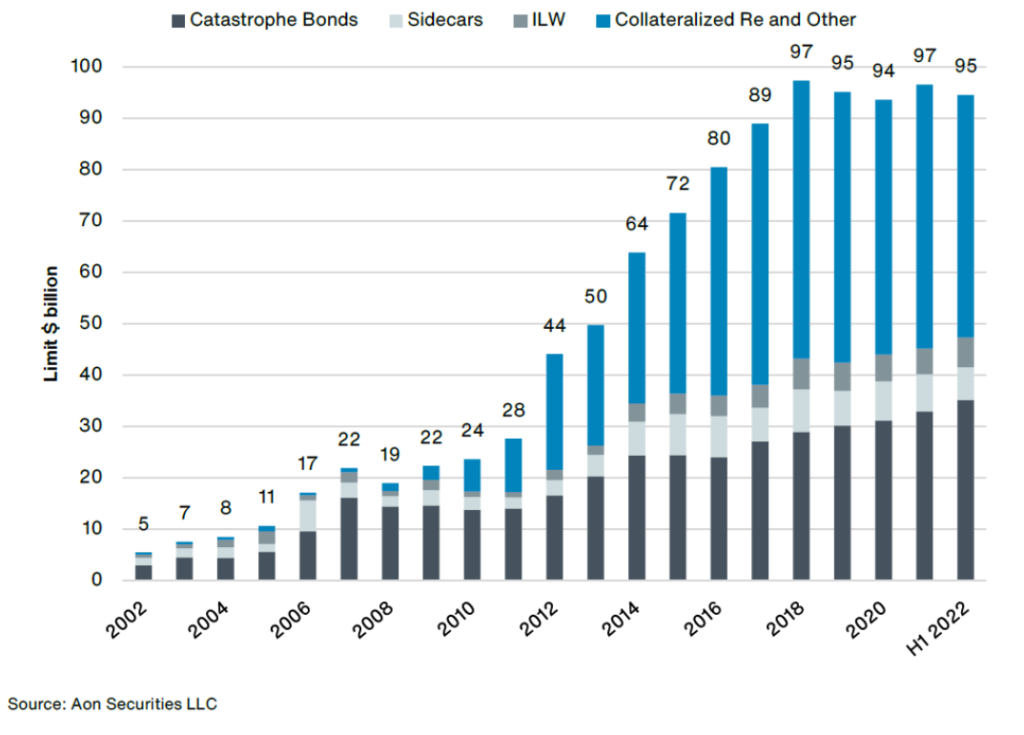

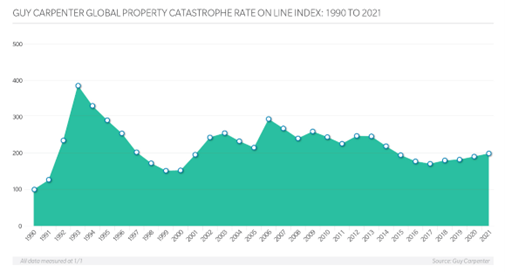

The following exhibits, while subjective, tell a typical story of how ILS capital inflows have impacted the market during the period 2011 to 2018, we have seen dramatic growth in the supply (from $28 to $97Bn) complimented by a fall in price as demonstrated in the Guy Carpenter ROL Index below.

(Aon Securities LLC, 2022)

Cat Bond issuance has increased steadily YoY during this period as have ILWs, with the steeper gains made in the Collateralised Re and Sidecar areas.

The period from 2018 to 2021, also saw a string of losses impact the Collateralised Re sector, Hurricane Irma, US wildfire and tornado events, European Floods, Winter Storm Uri and Covid-19 fuelled by a combination of climate change and increasing social inflation. Even where these events did not directly cause losses, they served to trap collateral needed to support renewals and reinvestment, which is an inefficient use of capital from an investment perspective.

Cat Bonds on the other hand largely escaped any impact from the smaller loss events, hence their development has continued unabated during the loss impacted period while Collateralised Re and Sidecars have contracted, generating a price recovery to 2013 levels in the ROL index.

2011 to 2018 was without doubt a buyers’ market, what the graphs cannot show is the slippage in terms and conditions experienced in Collateralised Re products, neither do they show the impact on the Retrocession market; a much smaller but important market given that many Reinsurers rely on the Retrocession programmes to help shape their underwriting strategy.

The Retro market is an area with opaque data and greater volatility, where capacity changes (as well as losses) are amplified in comparison to the Reinsurance space. So, while it generates superior returns, the volatility and data constraints mean that it tends to be approached with caution by ILS investors.

The proliferation of Pillared and Aggregate Products in the Collateralised Re sector during this period served to lower retentions and changed the purchasing motivation of buyers from one of capital preservation to results protection, or perhaps more cynically, bonus protection.

Lowering attachments and the spread of loss coverages in combination with increased frequency of loss events and social inflation has exposed ILS Investors to unexpected losses – Investors were sold on hurricanes and earthquakes and have been delivered wildfires and pandemics.

Flight to Quality

The consequence of a loss of confidence in Collateralised Re products has led to a flight to quality across the different market sectors.

While the amount of capacity dedicated to ILS has remained static in recent years, this has been underpinned by the growth of the Cat Bond sector while Collateralised Re has retracted.

Investors have a far greater understanding of the insurance space than they did 15 years ago, experience has replaced naivety and dedicated insurance investment professionals have spent their whole career working in the sector. Insurance as an asset class is attractive to investors. It is an uncorrelated investment in comparison to other asset classes, remains largely unaffected by movements in the wider equity markets and economy, representing a very low systemic risk.

The reaction of Investors to the current market conditions appears to be a realignment of interests into investments that provide greater clarity of coverage, certainty in outcomes and remoteness of risk. Features that are generally held by the Cat Bond product:

- Tend to sit at the top of the risk tower and is less susceptible to smaller cat losses

- More commoditised than Collateralised Re with defined perils and coverage

- High level of data granularity and clarity of information and portfolio exposure

- Independent verification of modelled losses and claims

- Most Cat Bonds are tradable on the secondary market, providing some element of liquidity

Therefore, it appears that in terms of ILS investment, Cat Bonds are in-vogue and are stealing market share from Collateralised Re, although the actual situation is more nuanced. This is because Cat Bonds and Collateralised Re are complementary products rather than competing, buyers cannot necessarily utilise a Cat Bond purchase to make a straight replacement for deficiencies from Collateralised Re products in their traditional reinsurance programme because:

- Cat Bonds can be time consuming and costly to arrange

- Cat Bond issuance requires underlying portfolios of size and scale

- A high level of data granularity and clarity is required, often not attainable for Retrocessionaires or Reinsurers with a high level of delegated interests

- Replacing low level protection with higher attachment changes the retained risk profile and financial mechanics

Additionally, there are other factors at play that are impacting the capacity crunch. Equity markets have responded by withdrawing credit (in terms of price valuation multiple) to companies that hold material exposure to excess property, i.e. catastrophe exposed insurance and reinsurance businesses.

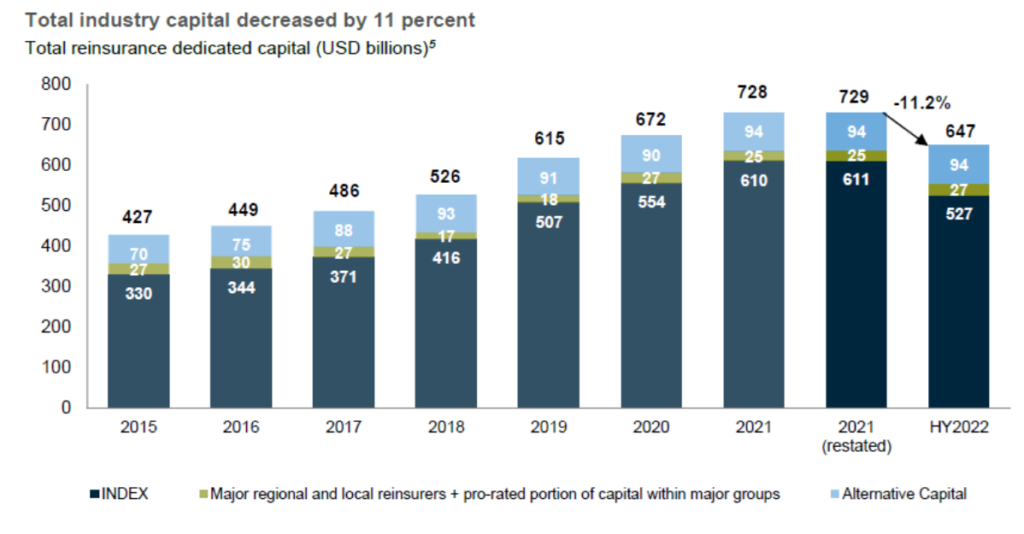

Consequently, several large, high-profile reinsurers have shifted underwriting strategies away from cat exposed reinsurance business and creating the largest retraction in reinsurance capacity seen in years, estimated at 11.2% in 2022 by Gallagher Re below, (although in fairness about half of this amount is attributable to investment losses):